The U.S. government just dropped a hammer on the most prominent name left in cryptocurrency (as if this week weren’t wild enough for the technology industry).

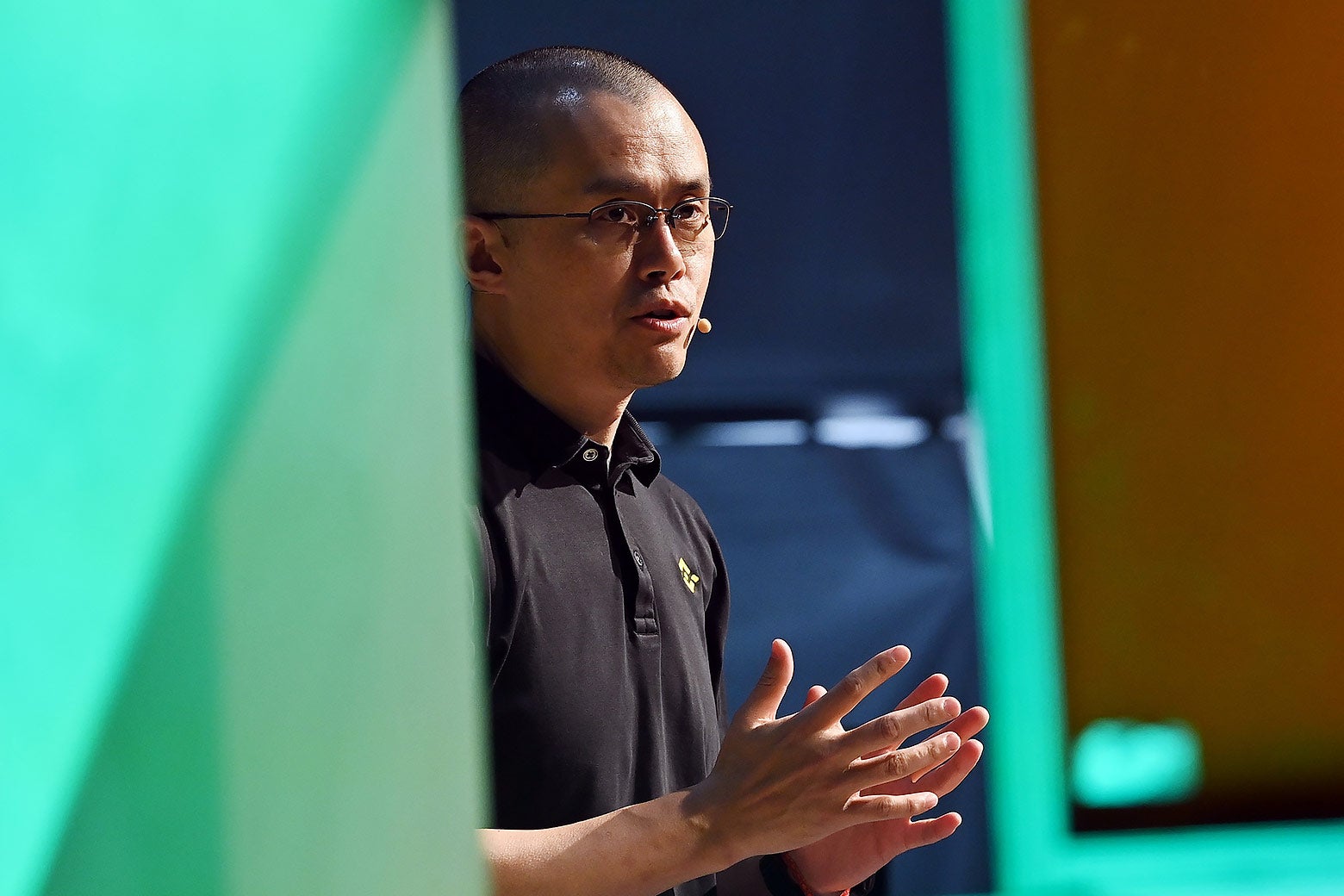

On Tuesday, Changpeng “CZ” Zhao, founder of Binance, the world’s largest cryptocurrency exchange, left his Dubai bunker to appear in a Seattle federal court, plead guilty to “one count of failure to maintain an effective anti-money-laundering program,” and pay a $50 million criminal fine. He also stepped down as company CEO. As part of the plea deal, his company Binance—itself charged with violating U.S. laws around money laundering, licensing for money transmission, and sanctions against Iranian transactions—is also paying $4.3 billion in fines to the Department of Justice, the Treasury Department, and the Commodity Futures Trading Commission. Happy Thanksgiving!

This wasn’t even the only rough news for crypto. Earlier on Tuesday, the DOJ said it was “seizing $9 million worth of Tether”—the dollar-pegged stablecoin that props up much of the cryptocurrency economy—in connection with “an organization that exploited over 70 victims through romance scams and cryptocurrency confidence scams.” This came just a day after Tether acknowledged it had worked with the DOJ to carry out “the largest-ever freeze of [Tether] in history,” after $225 million of its currency had been found circulating in a separate romance-and-crypto scam, this one linked to “an international human trafficking syndicate in Southeast Asia.” On Monday, the Securities and Exchange Commission also sued another well-known crypto exchange, Kraken, for failing to register its financial services with the government properly and commingling customer deposits with corporate assets. (Remind you of anyone else?)

Not long after CZ registered his plea, officials held a cross-department press conference on the actions against Binance, featuring Attorney General Merrick Garland, Treasury Secretary Janet Yellen, Deputy Attorney General Lisa Monaco, and CFTC Chairman Rostin Benham. In his opening statement, Garland announced the “criminal enforcement” his department was enacting in addition to the civil charges from Treasury and the CFTC. “Binance has agreed to plead guilty to willfully violating the Bank Secrecy Act, knowingly failing to register as a money-transmitting business, and willfully violating the International Emergency Economic Powers Act,” the attorney general declared, adding that the government was “requiring Binance to pay $4.3 billion in penalties and forfeiture,” making for “one of the largest penalties we have ever obtained from a corporate defendant in a criminal matter.” Further, the administration is imposing extra monitorship over Binance and requiring the company to go back through its past transactions so it can file reports on suspicious activity it had freely allowed on its exchange. What kinds of suspicious activity? According to Garland:

- Binance had fostered $900 million of transactions between American and Iranian users, even though these trades with the Middle Eastern country were subject to sanctions;

- The exchange also allowed for “millions of dollars” in sanctioned trades with users based in Syria and in Russian-occupied Ukrainian states;

- Beginning in August 2017, right when the platform came into being, various Binance traders collected a total of $106 million in Bitcoin from Hydra, the Russia-based darknet hub of illegal activity that was shut down by the DOJ and German authorities in April 2022;

- Binance engaged in business with another notorious money launderer, the crypto-anonymizing service Bestmixer, until the latter was forced to shut down in May 2019.

Garland also made clear that Binance employees had not only violated U.S. laws around financial-service registration but had pretended to comply while acknowledging privately they were doing nothing of the sort. The attorney general alluded to the creation of the Binance.US corporation in 2019, putatively. Hence, the exchange had a website that precisely followed stateside regulations while allowing its international branch to operate in the rest of the world. But even though “Binance blocked some U.S. users on Binance.com and redirected them to the U.S. exchange,” Garland explained, the international enterprise “continued to allow some of its most important, high-volume U.S. users to remain on the unregistered Binance.com exchange.” And more: “At the direction of Zhao and other senior leaders at Binance, employees encouraged their high-volume U.S. users to conceal their U.S. connections, including by creating new accounts that obscured their locations.” This was, CZ wrote privately, so that Binance could continue to grow—much of its trading had taken place in the U.S. from the jump—and reap the spoils from the two-year period in which it had no registered U.S. network. The CEO said it was “better to ask for forgiveness than permission.” Garland concluded with a statement directly aimed toward the crypto Wild West. “In just the past month, the Justice Department has successfully prosecuted the CEOs of two of the world’s largest cryptocurrency exchanges in two separate criminal cases,” he thundered, referring to the recently concluded case against Sam Bankman-Fried. “The message here should be clear: Using new technology to break the law does not make you a disruptor. It makes you a criminal.”

After Garland finished, Yellen stepped up to say her piece on the company whose name she pronounced “bih-NANCE.” “Over more than three years, FinCEN, OFAC, and IRS Criminal Investigation thoroughly investigated key aspects of Binance’s activities,” she began. Their findings: “Binance was allowing illicit actors to transact freely, supporting activities from child sexual abuse, to illegal narcotics, to terrorism, across more than 100,000 transactions. That includes transactions associated with terrorist groups like Hamas’s al-Qassam Brigades, Palestinian Islamic Jihad, al-Qaida, and ISIS. Binance processed these transactions but never filed a suspicious activity report. And it also allowed over 1.5 million virtual currency trades that violated U.S. sanctions.”

This called for what Yellen characterized as “the largest enforcement action in Treasury’s history,” with the respective Financial Crimes Enforcement Network and Office of Foreign Assets Control fines alone adding up to those above $4.3 billion. In addition, Binance will be forced going forward to instill “effective” money-laundering controls and subject itself to “increased scrutiny for five years through a third-party monitor” appointed by FinCEN—which will ultimately facilitate “Binance’s complete exit from the United States.” Binance could be subject to additional punishment if it fails to follow those conditions. “And let me be clear,” Yellen concluded. “We are also sending a message to the virtual currency industry more broadly, today and for the future: If virtual currency exchanges and financial technology firms wish to realize the tremendous benefits of being part of the U.S. financial system and serving U.S. customers, they must play by the rules. And if they do not, the U.S. government will take action.”

Monaco stepped up next to reiterate the Treasury secretary’s warning. “If you serve U.S. customers, you must obey U.S. law,” she insisted. “Crypto assets may be advertised as borderless, but the Department of Justice will enforce U.S. law across and throughout crypto markets, even in their darkest corners.” This was appended with a jab at Silicon Valley more broadly: “Some say the key to success in the tech sector is to ‘move fast and break things.’ Today’s actions show that if what you break is the law, there will be consequences.” After rubbing that one in, Monaco explained that these DOJ actions were part of a broader mission by the federal government to take on “the intersection between corporate crime and national security.” What did this mean? “Today, corporate crime undermines not only our markets and investors but also our national security. The laws we are enforcing today were designed to protect the security of our financial markets—and to protect our financial institutions from exploitation by terrorists and money launderers.” And yes, those laws applied as much to “decentralized and cutting-edge technologies” as they did to your typical big banks, thank you very much.

Finally, a word from the CFTC’s Rostin Benham, speaking to the charges his agency had filed back in March against CZ, Binance, and former Binance CCO Samuel Lin. In “resolving” those charges, the agency would impose a $2.7 billion fine upon Binance, a $150 million penalty against CZ, another $1.5 million fine against Lin, and consent orders on the executives. “Binance and its leaders sought to dupe and indoctrinate their employees and customers, building a cultlike following premised on circumventing their compliance controls to maximize corporate profits above all else,” Benham said. Further, it had never even registered with the CFTC—which, in resolving its eight-month-old case, had reestablished its “reputation as the proven leader in the civil enforcement space when it comes to digital assets.” If that was a shot at the absence of the publicly crypto-hostile SEC and at those who’ve dismissed the CFTC as being too cuddly with crypto—well, it remained a subtle one. “American investors, small and large, have demonstrated an eagerness to incorporate digital asset products into their portfolios,” Benham acknowledged as he drew close. But what if those digital-asset vendors broke the law as Binance did? “There is no question that the CFTC will strike hard and aggressively.” The CFTC’s other commissioners followed up with individual digital statements approving of their employer’s actions—with the notable exception of Summer Mersinger, the Biden appointee often recognized as crypto’s regulatory advocate thanks to her frequent dissents from the agency’s crypto decisions. As of this writing, Mersinger has not weighed in on CFTC’s decision.

All this, on top of Yellen’s comment to a reporter, declaring that “this is a regime that can support financial innovation—we will not end cryptocurrency transactions in the United States,” made it apparent that the federal government viewed its crackdown on Binance, in combination with SBF’s Nov. 2 conviction, as part of a far-reaching battle to snuff out criminality within cryptocurrency, but not strangle the tech itself. Still, the whole conference was undoubtedly a tightening of the leash. The U.S. government has officially smacked down the world’s biggest crypto exchange, clarifying that whether you are dealing coins made of copper or 1s and 0s, you are subject to the same laws; it was made especially clear following an explosive debacle around a misleading Wall Street Journal report on Hamas financing its militant activities through crypto, that digital exchanges could not get away with providing funds for terrorism; finally, it was characterizing crypto misdeeds as nothing less than a national security concern, making it subject to aggressive government scrutiny. In other words, the federal government’s war on cryptocurrency may yet become another arm of its never-ending war on terror. You don’t have to be a crypto lover to raise eyebrows at such rhetoric.

To be clear, it’s not a bad thing for the government to pursue crypto vigorously—by all accounts, whether in a bank or a wallet, Binance and some of its fellow exchanges (like FTX) have gotten away with defrauding everyday folks and enabling sketchy-at-best activities for too long now, and it’s only fitting to not only hold them accountable. Still, if even formerly crypto-friendly officials (Behnam and Yellen, for two) are talking like this, it’s no doubt a signal that the industry will face a lot more heat.

Which brings me to the SEC. The regulatory agency whose chair, Gary Gensler, has become nothing less than a sworn enemy of the crypto industry (including Binance), was notably not a party to Tuesday’s government settlements—meaning its eye-popping June lawsuit against CZ, Binance, Binance.US, and Binance.US’ parent company is still in motion. The commission appears not to have made any statements about Tuesday’s Binance news (it did not respond to multiple queries I sent). But, since the hearing over Binance.US’ motion to dismiss is scheduled for Jan. 19, it follows that the company (and CZ) has a protracted legal fight ahead of it.

Hardly ideal, considering Binance has spent the past year in panic mode thanks in large part to the SEC’s severe charges: misleading investors, laundering funds inappropriately, engaging in securities fraud, and wash trading (i.e., self-dealing in company securities to juice their value misleadingly), and mixing customer and corporate assets without due disclosure. (Another one!) It wasn’t just agencies; a bipartisan group of senators had also requested that the DOJ investigate whether the company had made false statements to Congress. Moreover, the U.S. regulatory crackdown occurred alongside other events of concern for Binance’s enterprise: the global crypto-market downturn that resulted from the fall of Sam Bankman-Fried’s FTX and Alameda Research firms (a demise ignited in large part by CZ himself) and the legal scrutiny that other nations brought upon Binance, endangering its licenses in Russia and France—and all but criminalizing its operations in Australia, Canada, Nigeria, the Netherlands, the United Kingdom, and Belgium, in succession. The overall fallout? Massive turnover in the C-suite, thousands of staff layoffs across international outposts, and billions of dollars of wealth gone poof.

Binance has consistently faced probes from various countries ever since it surged to the top of the global crypto industry in 2018, but it has never been battered so hard and so relentlessly until this year. With the Chinese-Canadian CZ now agreeing to stay far away from Binance for three years (part of which he’ll likely spend in prison, with a sentence to be determined six months from now), much of the U.S. government is formally closing myriad probes into Binance, long after the DOJ and the Internal Revenue Service began sniffing around in 2021. The CFTC, likewise, will drop its demand for a jury trial. (Sorry to disappoint all the readers who followed our SBF-in-court coverage!) Most reassuringly for crypto traders, Binance will not immediately shutter its stateside ops, thanks to a DOJ arrangement with the DOJ that will allow the company to keep running—under new management, of course, and within the bounds of strict legal compliance.

Speaking of new management, CZ tweeted Tuesday that he was appointing Binance’s global head of regional markets, Richard Teng, to replace him as head honcho, even as CZ remains the majority owner and an informal consultant, “consistent with the framework set out in our U.S. agency resolutions.” That would’ve been massive news even without the fanfare of government investigation. Changpeng Zhao has been one of crypto’s most important champions for a decade, having invested all his wealth in Bitcoin in 2013 and playing a pivotal role in launching the early exchanges Blockchain.info and OKCoin. His Bitcoin devotion persisted through the currency’s ups and downs, and his entrepreneurial ventures in the space—including the introduction of Binance in 2017—made him one of the world’s wealthiest crypto titans by 2018, according to Forbes. It’s difficult to imagine what the crypto space would look like today without CZ’s zeal, and more burdensome to envision what will become of Binance after his departure.

What’s next for CZ, then? Should he dodge any time behind bars? “I will probably do some passive investing, being a minority token/shareholder in blockchain/Web3/DeFi, AI, and biotech startups. … I can’t see myself being a CEO driving a startup again.” (U.S. regulators probably don’t see that, either.) CZ also threw another proud shot at the CEO he’d helped to consign to history approximately one year ago—Sam Bankman-Fried—by noting that his settlements “do not allege that Binance misappropriated any user funds, and do not allege that Binance engaged in any market manipulation.” Left unmentioned is that we have yet to see how the SEC case goes.

Also left unmentioned are answers to multiple questions about Binance—and crypto’s future. Pointing to a year-old CNBC clip that showed CZ waffling when asked if Binance could cover a potential $2.1 billion financial hole, famed short seller Nate Andersen—best known as head of the ruthlessly effective Hindenburg Research firm—cast doubt on Binance’s (and by extension, CZ’s) ability to cover the billions of dollars it’s committed to U.S. officials. The ongoing SEC case, alongside the agency’s concurrent suits against rival exchanges Kraken and Coinbase, will play a key role in determining which government actors oversee specific digital tokens in the future, whether those are named Ethereum or Cardano or Solana or whatever. (In response to Tuesday’s news, Coinbase CEO Brian Armstrong tweeted, “We now have an opportunity to start a new chapter for this industry.”) Also, we still have no idea what will come of the $500 million Binance pledged to Elon Musk to support his $44 billion Twitter takeover, significantly since the value of X/Twitter has since plunged to $19 billion.

Friends, it’s been an earth-shaking week for both A.I. and crypto—and it’s only Tuesday! Gobble gobble, am I right?